Akash Raigangar and Luke Baker from Planetary Scale highlight the growing focus on large-scale, First-Of-A-Kind (FOAK) projects in climate-tech innovation. These groundbreaking initiatives face distinct challenges, including securing funding, managing technological risks, and navigating complex operational processes.

Deploy, deploy, deploy has become the new rallying cry of the climate-tech world, reflecting both the excitement and urgency towards commercializing new climate technologies. Upcoming projects are breaking ground and hitting headlines frequently, as we witness a wave of early-stage climate-tech startups gradually approach their pivotal first commercial deployment (FOAK) moment.

This transition from early-stage technology development to FOAK is thrilling, but also very complex, and requires a significant shift in approach for founders. Beyond the obvious funding gap, executing a FOAK project presents entirely different challenges vs. those encountered during the conventional early-stage startup journey. It requires navigating a very different capital stack (project investors vs. VC), employing alternative entity structures (off-balance sheet), and collaborating with a new set of stakeholders (regulators, EPCs, etc.).

For climate founders, planning around these elements early-on with the big picture in mind (e.g., optimizing scale-up at each stage; building key commercial relationships from day 1) is critical to ensure success at the FOAK stage. In this series, we aim to share best practices/lessons learned from our experience working with climate startups on their journeys from seed to FOAK, and the broader commercialization of their technologies.

But first…what the ‘FOAK’ is FOAK?

FOAK, or First-Of-A-Kind, refers to projects that develop and implement the first commercial facility for a startup, after they have proven their technology at smaller scales. FOAKs are large-scale project-type investments, typically factories or plants for energy, manufacturing, or chemical processes, serving as proof-points for future commercial facilities. By definition, these projects carry more risk and higher costs vs. projects for more established technologies, due to their novel/untested nature, but are a necessary first step in commercializing new climate technologies.

Monolith’s Olive Creek methane pyrolysis FOAK facility (Image Source: Monolith)

FOAK projects are large-scale engineering undertakings, encompassing the

end-to-end lifecycle (planning, building, deployment and operation) of this first commercial facility. This includes processes such as site selection, permitting, design, engineering, construction, testing, and commissioning. CTVC offers an insightful checklist here that explores the key elements of FOAK projects and provides practical guidance on how to effectively prepare for each stage.

FOAKs are typically structured as standalone project entities (ProjectCo) to isolate the startup company from the project’s financial risks and liabilities. This off-balance sheet approach allows investors to invest directly in the FOAK project and its underlying assets, which retain some value independent of the startup’s performance or technology’s commercial-scale viability, thus simplifying and reducing overall risk for the investor.

Most FOAK projects typically fall in one of three use-case categories (shout-out to Deanna Zhang for this useful framework):

- Commercializing a set of large-scale chemical processes

E.g., OXCCU’s sustainable aviation fuel plant (Saltend, UK) and H2 Green Steel’s renewable hydrogen-based mill (Boden, Sweden). - Deploying large “chunky” asset installations

E.g., Fervo’s (first commercial-scale) 400MW geothermal plant (Beaver County, Utah) and Cobra Group’s Kincardine floating offshore wind farm (off coast of Scotland). - Manufacturing, assembling, & processing large volumes of produced goods

E.g., Tesla’s first commercial production facility (Fremont, California) and Northvolt’s ETT battery production plant (Skellefteå, Sweden).

Climeworks’ Orca FOAK Direct-Air-Capture plant (Image source: Climeworks)

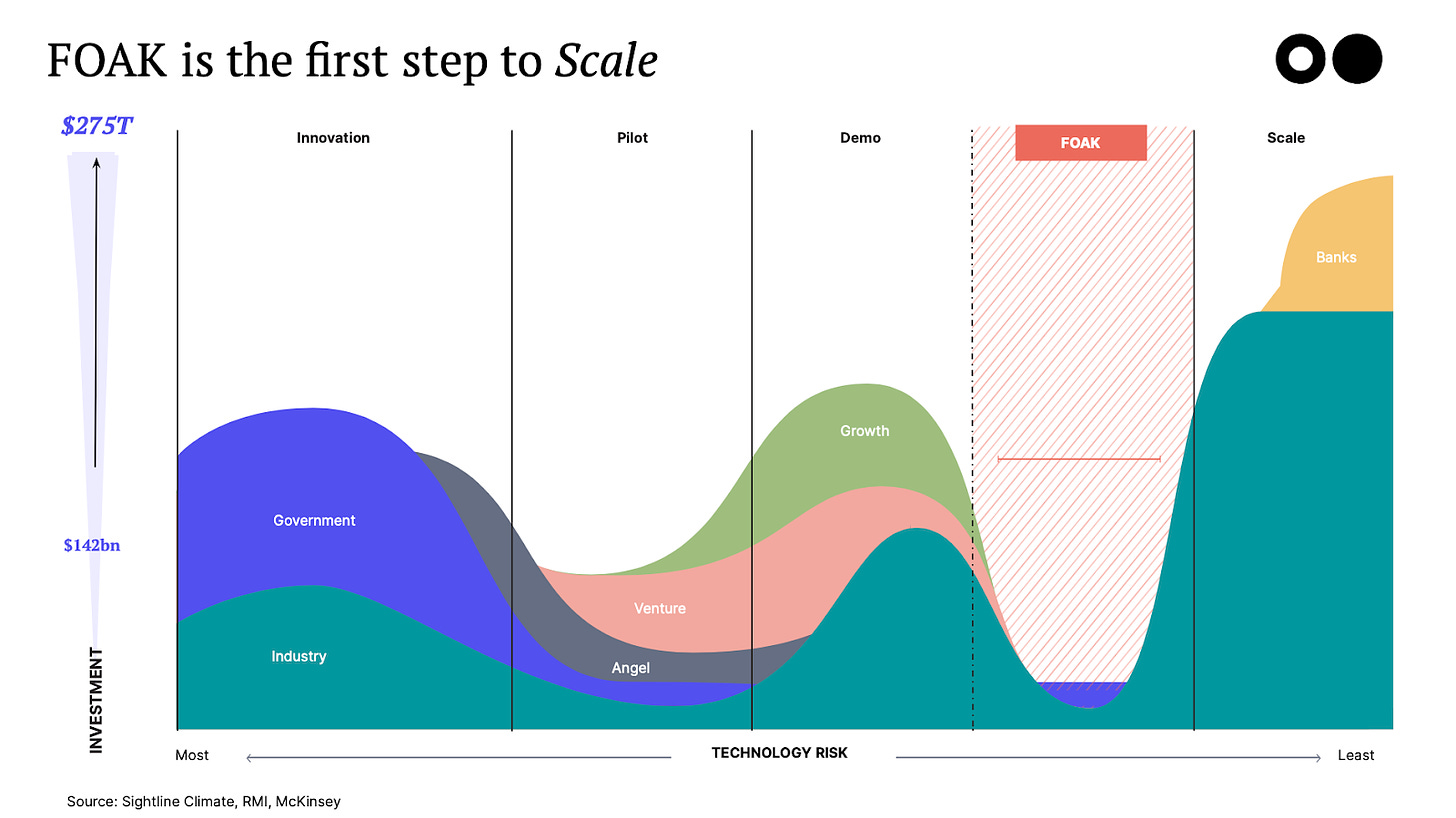

The Capital Landscape: Financing FOAKs

As a climate-tech startup approaches the FOAK stage, one of the biggest learning curves for founders is navigating a vastly different financing landscape compared to conventional early-stage startup fundraising.

In the early stages, climate startups primarily rely on VC dollars (and in some cases, grants). VCs typically invest smaller checks, based on a startup’s long-term vision, with the aim of maximizing upside potential while tolerating considerable downside risk. This makes them ideal partners at the early stages, when climate-tech startups raise smaller rounds (likely <$20m) to mainly fund R&D (proving technology at lab, demo, or early commercial scales). In the later stages (when tech is proven at scale), climate projects can access a deeper pool of traditional investors (e.g., infra funds, PE, banks) who prioritize more predictable returns, and are willing to forgo high upside potential to minimize downside risk. This capital tends to be much cheaper, but demands a very low-risk profile in return.

However, during the mid-stages, climate founders often face the dreaded valley-of-death when fundraising for their FOAK facility. At this point, capital needs are significantly higher than earlier rounds — $50-100m in many cases, to fund complex engineering and construction — but the technology and business model remain unproven at commercial scale. This places FOAK projects in a challenging middle ground, where they require large-scale capital investments (that likely only traditional investors can provide), while carrying risks more typical of venture investments. This leaves these projects stuck between two distinct asset classes with differing risk and return expectations – thus leading to a funding gap.

(Image source: CTVC article Venture to Project Finance Duolingo)

Despite this, the financing options for FOAK are expanding rapidly, and the blending of various capital sources has emerged as a winning strategy. This approach involves structuring each investor’s contribution to align with their risk/return preferences while also fitting with the capital needs/terms for the project at the aggregate level. In particular, blending commercial sources (e.g., emerging infra funds, corporate balance sheets) with more concessionary sources (e.g., catalytic funds, philanthropic organizations, government loans) is common at the FOAK stage; this mix allows concessionary sources to absorb a larger portion of the project’s risk, thereby enabling the commercial investors to meet their risk/return expectations.

On the same principle, another approach to financing FOAK projects involves combining debt and equity at the project level, often alongside equity investment directly into the startup as well. This structure enables more effective risk distribution and offers investors the potential to benefit from the startup’s upside, while also improving the project’s capital accessibility.

As a result of these innovations, many sources within the larger climate capital stack are now participating in the FOAK stage (commonly in a blend with one another), bridging the gap between VC at the early stages and traditional investors at the later stages. Some of these (referred to as “FOAK investors” in this series) are listed below (watch out for our upcoming post on navigating the FOAK capital stack):

- Emerging project investors (debt and equity), such as Spring Lane Capital and Keyframe Capital.

- Large corporates and strategics in sectors related to the project/technology, such as Aramco and Nestle.

- Development finance institutions and export banks, such as World Bank IFC, IREDA and ERBD.

- Government loans and programs, such as the various grants/tax credits available through the Inflation Reduction Act and from the European Investment Bank.

- Philanthropic and catalytic funds, such as Breakthrough Catalyst and Prime Coalition.

Navigating Risks: Making FOAK Projects Attractive to Investors

FOAK projects, while groundbreaking and essential for climate progress, often come with a unique set of risks that can deter potential investors. Understanding and mitigating these risks (often by making the right strategic decisions from the early stages) is essential for founders aiming to make their FOAK projects financeable.

As a climate startup advances from early to later stages, its risk profile evolves, reflecting the perspectives of the primary investor group at each phase. At the early-stages, VCs prioritize upside potential and thus evaluate risk based primarily on market size and a team’s ability to capture it. In contrast, later-stage traditional investors (infra funds, PEs, banks) adopt a more structured approach, focused on meeting a target rate of return while minimizing risk of loss.

FOAK investors, particularly emerging project investors, operate similarly to traditional investors in terms of evaluation processes/criteria, but typically have a higher risk appetite. These investors evaluate a wide variety of a project’s attributes (market viability, technology, costs etc.), but do so primarily through a risk lens. The most useful way for climate-founders to understand these risks is to categorize them across 3 key groups: market risk, technology risk, and execution risk.

Stay tuned for our future deep-dives and case studies on many topics introduced below, including best practices for optimizing technology scale-up at each stage and gold-standard approaches to financial modeling for FOAK projects.

- Market Risk

A project’s marketability is the starting point in an investor’s project evaluation. Securing investment into a project, especially at the FOAK stage, is nearly impossible without providing clear evidence of market validation and binding commitments. This is best demonstrated through offtake agreements, which help guarantee revenue streams and establish credibility for a project’s financial projections. Gold-standard offtake agreements typically incorporate attributes such as a take-or-pay structure and a clearly defined product-spec – watch out for our deep-dive on best practices for structuring off-take agreements. - Technology Risk

FOAKs inherent carry more technology risk than traditional infrastructure projects, due to their untested technologies and novel processes. To build investor confidence, it’s crucial to validate the technology in terms of product & process reliability (consistent conversion of inputs to outputs, output quality etc.) at each development stage. In addition, choosing an appropriate scale-up factor between stages is crucial to ensure core technological processes continue to behave as expected and that sufficient high-quality performance data is gathered (as proof points for investors) at each stage. Watch out for our upcoming piece on navigating scale-up and ensuring sufficient validation across each TRL/developmental stage. - Execution Risk

Investors also assess the operational challenges associated with bringing the project to fruition, focusing on the team’s ability to de-risk execution and the degree to which risk can be offloaded to the third-parties involved. One of the primary areas of execution risk lies in the relationships and contracts with key stakeholders (EPC contractor, OEMs, landlord etc.) involved in the project’s development/operation. Partnering with the right suppliers from day one (those with high reliability and creditworthiness) and structuring contracts that match the project’s needs and debt conditions is crucial to minimize supplier risk in execution. Stay tuned for our upcoming deep-dive for more details on de-risking supplier relationships and project execution in the FOAK context.

Summing It Up

Until very recently, it was rare for venture-backed startups to venture into FOAK projects. While FOAKs are becoming more common in today’s climate-tech landscape, we’re all still collectively figuring things out as we go — the FOAK playbook continues to evolve.

Planning, developing and executing a FOAK will never be “easy,” but the evolving climate ecosystem (including support from governments, expanding capital landscape and increased corporate participation) is making the process less complex day-by-day.